Another year, another Cannes Lions Festival of Creativity in the books

Another year, another Cannes Lions Festival of Creativity in the books.

The CTV ad market is worth $38 billion — yet most brands still lack the visibility to know if their campaigns are working. Here's what's broken, and what it takes to advertise smarter on CTV.

By 2028, connected TV advertising will surpass linear for the first time in history. That’s not a prediction – it’s a consensus. U.S. CTV ad spend hit $33 billion in 2025 and is on track to reach $38 billion this year, according to eMarketer1. Meanwhile, CTV already captures 20% of daily media time among adults – but only 8% of total ad spend2. That gap between where audiences live and where dollars go isn’t an opportunity. It’s a warning sign that something, structurally, is not working.

The CTV pitch has always been compelling: the premium attention of TV, combined with the precision of digital. Big screen. Sound-on. Real people. Full control.

The data backs it up. CTV ads drive the highest attention scores and achieve completion rates between 90% and 98% – compared to 20-40% for YouTube and often below 30% for social media3.

But why does this require 40% of advertisers still working across five or more CTV providers on a typical campaign?4 Why does 37% of advertisers cite frequency management across publishers as a top CTV challenge?5

And why – despite premium inventory, high attention, and measurable outcomes – does only 30% of advertisers have full visibility into where their ads actually run?6

What’s broken in CTV isn’t the channel. It’s the way the industry has chosen to sell it.

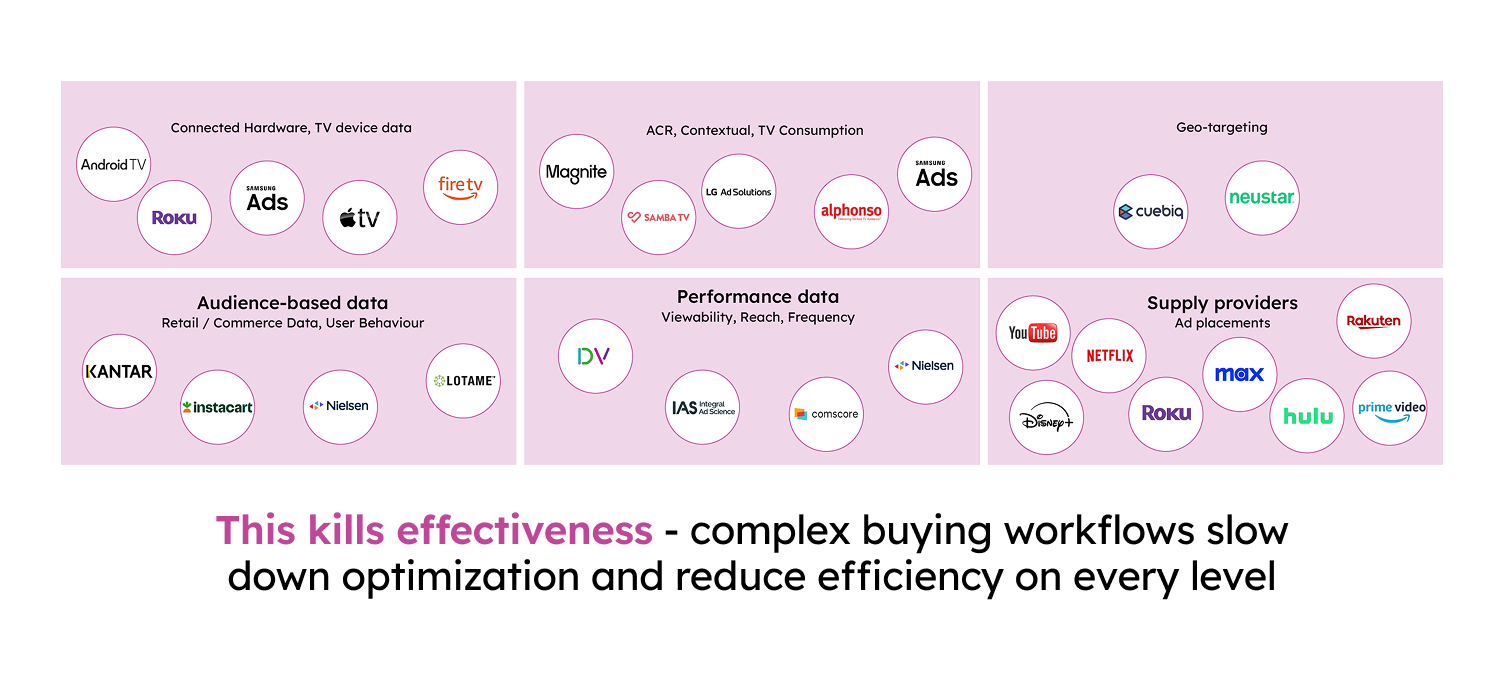

CTV inventory is spread across dozens of platforms – Netflix, Prime Video, Disney+, Tubi, Pluto TV, and hundreds of apps in between. Each operates its own data silo. And the data flowing through this ecosystem – device signals, content metadata, audience identifiers, location – is aggregated and processed by multiple other entities before it reaches a buyer. And at every handoff, something gets lost: transparency, efficiency, or both.

This is what creates the mess. IAB data shows that fragmentation ranked as the number one challenge CTV advertisers want providers to address in 2026 – ahead of measurement inconsistency, fraud, and ad placement transparency.7 Nearly all advertisers say they see value in managing CTV through a single platform – and yet the market continues to push in the opposite direction.8 Why? Because more fragmentation is good for the platforms. More partners, more fees, more complexity – and with complexity comes dependency. The incentives don’t align with the buyer.

The result is a channel that punishes brands for scaling ambition. The more CTV you try to buy, the more publishers you add, the more your frequency spirals, your attribution blurs, and your actual understanding of what you bought shrinks.

That’s the uncomfortable truth: the industry hasn’t solved CTV complexity. In most cases, it’s just charging you to navigate it.

The question every media buyer should be asking right now isn’t “should we invest in CTV?” They should. The question is: are you buying it in a way that actually works?

Brands need a unified tech stack – not a patchwork of vendors. Impactful CTV activation shouldn’t require assembling a fragmented stack of publishers, targeting solutions, verification vendors, measurement tools, and creative partners, and then manually reconciling their outputs. The question to ask about your current setup is: do all of these things talk to each other in real time? Managing this in-house is expensive, technically complex, and almost never done well at the brand level. The operational cost and expertise gap is exactly why choosing a single partner that has built around holistic campaign infrastructure – not just sold you access to inventory – is the meaningful decision.

Unified targeting signals – not glued-together packages. The industry is moving in a clear direction on this. In late 2024, IAB Tech Lab released new CTV genre guidance, introducing standardised genres attributes to help buyers accurately read content context across publishers – specifically to avoid misclassification, inefficiency, and targeting failures.9 Genre is a more stable, durable, and privacy-safe targeting signal – because it tells you what someone is watching right now. Reaching a potential Bridgestone prospect while they’re watching an automotive show isn’t a coincidence; it’s timing. And timing – real-time context – is what separates a relevant ad from an intrusive one. Adlook’s research on bid request data shows that across key markets, between 54% and 82% of CTV impressions contain genre data, making it the most consistently available and actionable human signal in the bidstream.10

Cross-platform reach, frequency control, and cross-device attribution. These are not measurement luxuries – they are the operational minimum for a channel that reaches multiple platforms, multiple devices, and multiple household members simultaneously. Without deduplicated cross-platform reach, you don’t know your true campaign footprint. Without frequency control, you’re wasting the budget that was supposed to build brand affinity. And without cross-device attribution, CTV sits in your plan as an upper-funnel black box, judged on expensive brand lift studies rather than the business outcomes it’s capable of driving. Adlook’s CTV-to-website attribution data shows that between 1 and 5% of households exposed to a CTV ad visit the advertiser’s website within 14 days11 – a measurable, attributable business signal that changes the conversation from “awareness channel” to “performance contributor.”

Creative that activates the screen. CTV creative is no longer just a 30-second brand spot. It’s a QR code that drives your viewers directly to a product page while they’re still watching. It’s an interactive video where viewers respond to the ad using their remote – selecting options, exploring products, playing with your product – without leaving the viewing experience. It’s genre-tailored executions where you aren’t running the same generic spot, but creatives adapted to the emotional context of the content around it. The big screen became interactive. The question is whether your creatives are built to take advantage of that.

Transparent reporting – not black boxes. If your CTV report doesn’t show you granular delivery insights (e.g. genre, UGC vs professional, series, time, geo heatmap) and full publisher list – you’re not managing a CTV campaign. You’re managing a promise. Impression-level transparency isn’t a premium feature. It’s the baseline for informed optimisation, and it’s the only way to verify that your brand safety standards are being met at the placement level.

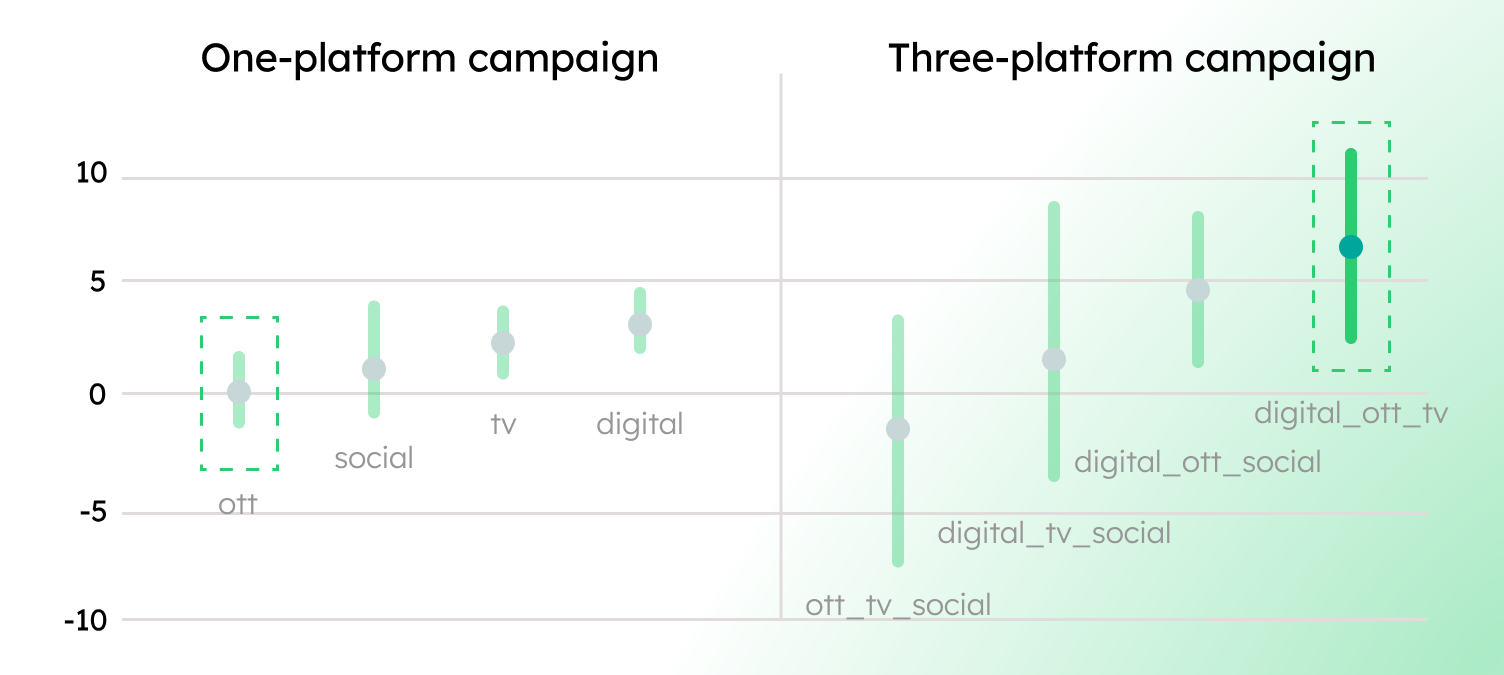

Here’s a finding that doesn’t get enough attention: CTV’s single strongest performance multiplier isn’t your targeting strategy or your creative. It’s omnichannel context.

Comscore’s Brand Lift Study analysis showed that three-platform campaigns combining CTV, digital video and linear deliver meaningfully greater brand lift than single-platform CTV buys – and that CTV adds substantial incremental reach to linear TV, meaning each touchpoint reaches audiences the others don’t.12

This is why treating CTV as an isolated channel – a “TV replacement” bolt-on to a digital plan – consistently underdelivers on its potential. CTV performs when it’s integrated: when targeting uses the same content signal across CTV, web, and app environments; when creative tells a consistent story adapted to each screen and context; when measurement connects exposure across devices to a single attributed outcome.

CTV delivers what it promises: a lean-back, full-screen, high-attention environment.

The brands winning with CTV in 2026 are not the ones with the biggest CTV budgets. They’re the ones who stopped assembling CTV from pieces and started demanding a unified approach: one tech stack, one targeting methodology, one measurement framework, one creative strategy.

If your CTV plan still looks like a list of vendors, you are not planning CTV. You are managing inventory.